MAKE HISTORY: A Rare Feature in 26 Years…

MAKE HISTORY: A Rare Feature in 26 Years…

I like to do interesting things.

I find that intellectual liberty helps one get closer to achieving an impeccable body of work, truth, and market wisdom.

Here is the front page of The Morgan Report…

For readers who may have missed the context of this team-up, you can read it below here.

*special preview

Outer Limits of the Global Minefield

By Peter Pham

In these turbulent times, it’s crucial to rely on first-principal insights to navigate the upheavals orchestrated by central planners. My goal is to equip you with the essential tools and knowledge to discern the battles affecting our body, mind, and soul, enabling us to safeguard and thrive in our individual sovereignty.

Governments are expanding their size by imposing escalating debt burdens on their citizens, narrowing the political Overton window, and accelerating centralization. In 2023, global government debt reached $97.1 trillion, marking a 40% increase since 2019 in the post-COVID-19 lockdown world or 330% of global GDP. This lamentable reality persists because many developed governments swiftly seize tax revenues exceeding $6 trillion in the USA to finance their ideological, non-absolutist stances on geopolitics and social issues, striving to become “too big to fail.”

Consider this: As individuals and households filed their taxes on April 15th, contributing almost 90% of US tax revenue, corporations accounted for just 10%. On April 20th, the US House of Representatives passed a bipartisan $95 billion foreign aid bill for Ukraine, Israel, and Taiwan. Then on April 23rd, the US Senate swiftly approved the bill, marking a quick legislative process in and out!

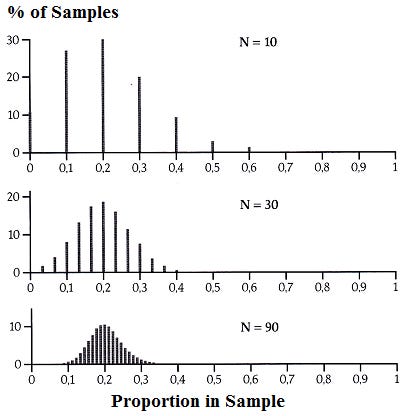

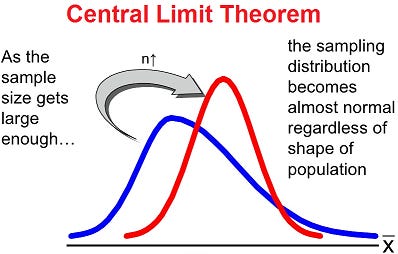

The dynamics of Hegelian dialectics and the Overton window contribute to the rise of big government, as evidenced by government debt and spending, which are rooted in the central limit theorem. This theorem states that the distribution of samples tends to form a normal distribution as size or time increases, irrespective of the initial conditions.

Central Planning Theorem

I’ve observed that regardless of a government’s initial form, whether authoritarian or democratic, the central limit theorem suggests that all governments will inevitably expand in depth and size, leading to what we commonly term ‘big government’, similar to an expanding normal distribution. This illustrates the underlying cause and necessity of the debt-fueled centralization we are experiencing. It follows a common historical pattern seen in the rise and fall of empires. Examples include the fall of the Western Roman Empire in the 5th century, the collapse of the Soviet Union in 1991, and the structural shifts of the American empire. Excessive debt and centralization have historically contributed to the rise and downfall of great powers throughout history.

In recent years, the US federal government’s spending has ranged between 20-22% of GDP, surpassing the optimal level of around 17.45% of GDP, where government spending maximizes economic growth. In contrast, at its zenith in the late 19th century, the British Empire’s government spent approximately 10-15% of GDP. Similarly, historical empires such as the Roman Empire also maintained relatively smaller governments compared to modern standards.

However, none of the previous empires have expanded to the extent in sheer breadth and depth as the modern-day central bankers. The total sovereign bond market is valued at over $119 trillion, with the American bonds making up over 39%. This ‘too big to fail’ system provides a compelling reason to support the idea that America is on a path to last as long as the average empire does, which is 400-500 years.

The New Normal

This is why I believe that we often misinterpret the many false flags of social and political instability as signals of the imminent downfall of the empire, which could potentially impact stock market performance and returns, leading to a crash. Current events such as student protests, world wars, central banking hubris, and controversial elections lead us to believe that a collapse could happen at any moment. However, both macro and micro data indicators reinforce centralization, which ensures the overall political stability of the government, as measured by the expanding sovereign debt market, and keeps stock markets near all-time highs. It’s worth noting that the S&P 500 has recovered from 5% drawdowns 239 times since 1927. This trend persists until the out-of-sight, out-of-mind tail-end risk emerges, or a black swan event occurs.

By expanding the size of government year after year, central planners push and prolong tail-end risk, emerging as the true masters of time. Through fiat money printing, even with erosion of marginal productivity gains, they effectively purchase time or extend tail-end risk as the size of the normal distribution or ‘big government’ expands, as emphasized by the central limit theorem. The trends of fiscal and monetary policy will become repetitive and predictable for us if we are willing to count the frequency. This practice keeps the deep state, bad banks, zombie companies, and ghost towns afloat for an unnaturally long period of time, regardless of the cost, just look at Japan.

Masters of Time

It's crucial to remember that all financial analysis and economics, whether directly or indirectly, measure time or follow a time series. Therefore, the central planners' perceived conquest of time, epitomized by clichés such as 'QE into infinity’, can be seen throughmarket signals.

The act of buying time from the inevitable ‘fall of the empire’ only exacerbates unnatural distortions and inversions. Positive economic data, seemingly disconnected from the real economy, such as changes in the job market, inflationary pressures, and company profitability ratios, underscore the widening gap between financial indicators and the actual economic landscape. If the tax-to-GDP ratio remains above 20%, the government appears content.

Corporate earnings on Wall Street in key sectors of our economy, or what Vladimir Lenin referred to as the “commanding heights” of the economy, such as ‘Big Banks’, ‘Big Tech’, ‘Big Pharma’, ‘Big Oil’, etc., reaffirm the objective of central bank monetary policies behaving as constituents and fueling big government centralization. It is the ‘Big Banks’ that rank among the top three buyers of government bonds through the deposits of individual taxpayers and corporations. This setup gives central planners the confidence to issue and manage debt with our tax revenue and orchestrate bond issuance demand from ‘big banks’ and central banks worldwide.

Centralization or federalization exacerbates the decline in benefits from the real economy, traded for a false sense of increased social welfare and protection through a vast network of government programs and departments, while the financial economy or stock market reaps the actual benefits and gains. The phrase “don’t bet against America” encapsulates the enduring strength and resilience of the US economy, which has seen remarkable long-term gains in equities like the Dow Jones, up over +38,000% since inception. However, the current focus on capital gains and unrealized tax gains underscores the evolving landscape of government finance and centralization.

Central Planning Necromancers

By securing taxation and bond issuance subscriptions with ideological centrism representation through tools such as the media, central planners can mimic the spirit of Rothschild geopolitically. This approach mirrors the Rothschild family's historical strategy of financing both sides in conflicts, ensuring profitability regardless of the outcome.

This method of dual investment allowed them to maintain influence and gain financially, irrespective of which side emerged victorious. Such financial maneuvers have been integral in shaping geopolitical landscapes, similar to how modern central planners might use media to influence public opinion and secure taxation and bond subscriptions, thereby stabilizing their power and control.

The conjuring of these ideological links to new trends in warfare involves conflicts fought through the manipulation of multiple economic, political, social, and military forces across various domains to achieve specific goals or circumstances. It emphasizes the use of deliberative manipulation to influence actors, networks, institutions, states, or any other force to achieve a goal while avoiding or minimizing retaliation. It’s akin to magic and appears almost magical due to its secretive, manipulative, and often invisible nature. Operating below the threshold of our observation makes real-time detection and attribution difficult today.

For Your Eyes Only

That’s why I want to draw your attention to cybersecurity within the expansive network of government departments and agencies. CrowdStrike has been making strides in the market, increasing its overall market share to about 9.95% as of Q4 2023. In that quarter, CrowdStrike’s revenue surged by 32.41%, far surpassing the average revenue growth of its competitors, which stood at 14.54%. The majority of CrowdStrike’s customers, approximately 62.72%, are in the United States, with other key markets including the United Kingdom (6.07%) and Australia (5.41%) - the five eyes.

At the core of CrowdStrike are Endpoint Protection Platforms (EPPs), which form the foundation of endpoint security. They examine files as they enter the government’s network and leverage cloud-based threat intelligence. CrowdStrike Falcon’s endpoint security protecting the centralized big government apparatus, making up 78.23% of revenue.

This is particularly crucial with the impending controversial presidential election on the horizon. CrowdStrike, the leading cybersecurity firm specializing in protecting elections and election infrastructure from cyber threats, has also warned that foreign adversaries like Russia, China, and Iran are likely to target the 2024 US elections with disinformation campaigns, cloud-based attacks, and the exploitation of AI technologies.

The War Time Economy

The current landscape, marked by proxy wars, tit-for-tat escalations, and the looming specter of a world war, has created a perfect storm for the defense industry, with governments around the world pouring billions into military spending. Global military expenditure reached a record high of $2.4 trillion in 2023. The United States accounted for 37% of this total, spending $916 billion on defense in 2023.

At the heart of this conundrum lie the foreign policy decisions of the United States government. Who previously injected $28 billion into post-Soviet Russia, then sent $111 billion in aid to Ukraine to fend off the Russian invasion of 2022. This has been a significant driver of increased defense spending.

Meanwhile, the U.S. has maintained a policy of “strategic ambiguity” regarding Taiwan, not committing to anything besides a ‘One China Policy’ that has led to a total accumulated trade deficit with China of several trillion dollars since normalized relations in 1979. Playing both sides comes with a history of sending over $22 billion to Taiwan amidst heightened tensions in the Taiwan Strait.

Driven by trends in warfare and fueled by fear-based media narratives, these policies have resulted in the sacrifice of lives and the emerging potential for a prolonged, costly proxy war that could escalate beyond control. They underscore how the actions of the U.S. government, echoing strategies akin to those of the Rothschilds, have directly or indirectly contributed to the worsening global situation in the real world, with the specter of a devastating world war looming ominously.

A Good Offense is Good Defense

The defense sector has emerged as a major beneficiary of the U.S. government’s spending spree. The country’s defense budget accounts for nearly 40% of global military expenditures, outspending the next nine countries combined. This surge in defense spending has translated into lucrative contracts for major defense contractors, with the top five U.S. defense companies (Lockheed Martin, Boeing, Raytheon, Northrop Grumman, and General Dynamics) earning a combined $174.5 billion in revenue in 2023.

Countries in the Middle East and Asia have also been increasing their orders to counter the perceived threats from China and Russia. This has resulted in a significant boost in sales and profits for U.S. defense companies, which have even been supportive of Boeing as they go through a transition with Defense, Space & Security revenue reaching $6.95 billion, beating the estimated $6.38 billion.

Riding Until the Wheels Fall Off

Despite being a much-criticized company, Boeing products averted a potential nuclear catastrophe a few weeks ago. The Israeli military employed its two primary defensive weapons, the Iron Dome and the Arrow 3, to neutralize the majority of the over 300 drones, ballistic missiles, and cruise missiles that targeted its territory.

Boeing successfully raised $10 billion from a bond sale a few days ago, with the sale being oversubscribed eight times, indicating strong demand from investors. The proceeds will bolster Boeing’s liquidity to address its existing debt maturities, including $4.3 billion due in 2025. Using oversubscription as an indicator and demand as a feedback loop for confidence in the company, especially in light of their $529 billion plus backlog of orders.

Of course, it’s the major banks and institutions, such as Vanguard Group Inc., BlackRock Inc., and Newport Trust Company, LLC, owning and buying Boeing’s debt, totaling over $63.58 billion, that play a crucial role in Boeing’s financial structure. ‘Big Biz’ uses the same model as ‘Big Gov’, growth from ‘Big Banks’ leveraging depositor capital to buy corporate and government bonds, resulting in the financialization of debt instruments becoming the core business.

Understanding the strategy and tactics conducive to centralization can indeed provide an edge in navigating the system effectively.